Electric vehicle insurance premiums are notably higher than those for traditional cars due to EVs’ higher purchase prices and costly battery replacements. Specialized parts, the need for trained technicians, and limited repair networks further contribute to increased costs. Comprehensive policies with battery protection, zero depreciation, and roadside assistance are crucial for EV owners to mitigate potential financial burdens.

Chief Economist and Data Scientist, Dr. Michel Léonard

Recent tariffs issued by U.S. President Donald Trump are on track to increase the price of parts and materials used in repairing and restoring property after an insurable event. Analysts and economists, predict these price hikes will lead to higher claim payouts for P&C insurers and, ultimately, higher premiums for policyholders.

After making several announcements since early March 2025, on April 2, President Trump signed an executive order imposing a minimum 10 percent tariff on all U.S. imports, with higher levies on imports from 57 specific trading partners. A general tariff rate became effective on April 5, while tariffs on imports from the targeted nations, ranging from 11 to 50 percent, took effect on April 9. A 25 percent tariff applies to all steel and aluminum imports and cars. President Trump says he might consider a one-month exemption to the auto industry, but as of this writing, no changes have been issued.

Generally, tariffs can bring in revenue for the issuing government but lower the operating margin for impacted domestic businesses. Inventory and supply chain managers may attempt to stockpile in advance of the new rates becoming effective, which in turn can spike demand and quickly spike prices for sought-after items. Eventually, these cost hikes get passed on to consumers.

Nonetheless, to ride out the situation, inventory and supply chain managers need a fundamental level of predictability regarding what the levies will cover, what the rates are, and when these rates go into effect. The timing and scope of President Trump’s tariff policies have been challenging to nail down, including for many goods particularly relevant to construction and auto manufacturing. For example, his initially declared rates for major trading partners – Canada, Mexico, the European Union, and China – have fluctuated as these nations announced reciprocal tariffs, and those levies, in turn, were met with higher US rates.

Then, on April 9, President Trump declared a 90-day pause on tariffs. This change was actually not a true pause but a reduction of previous rates for several countries to 10 percent, except for China. The White House has declared on April 10 that the previously announced 125 percent rate against goods from China is actually now 145 percent.

According to S&P, the levy on auto industry imports has been comparatively less dynamic as, despite confusing announcements from the White House, there has been no change to President Trump’s 25 percent rate declared on March 26, “which applies to all light-vehicle imports, regardless of country. The 25 percent tariff includes auto parts as well as completely built up (CBU) vehicles. The CBU autos tariff went into effect on April 3, 2025, while the auto parts portion is due to come into effect on May 3, 2025.”

As insurers grapple with risk management and inflationary pressures, other challenges posed by the tariffs can include issues for policyholders, specifically coverage affordability and availability. One downstream side effect may be the increased risk of expanding the protection gap – uninsurance and underinsurance (UM/UIM) due to higher premiums and higher valuations that can come into play when materials costs rise. Across the fifty states and the District of Columbia, one in three drivers (33.4 percent) were either uninsured or underinsured in 2023, according to a recent report, Uninsured and Underinsured Motorists: 2017–2023, by the Insurance Research Council (IRC), affiliated with The Institutes.

Our Chief Economist and Data Scientist, Dr.Michel Léonard, shares his analysis of how the tariffs may impact the P&C Insurance industry.

“There’s no crystal ball”, say Dr. Léonard, “but prudent risk underwriting and risk management suggests the use of scenarios and increased price ranges for different tariff levels, the more precise impact of which can be updated based on actual price increases for individual prices.”

Dr. Léonard outlines three types of P&C replacement cost scenarios given different tariff ranges:

1) For single-digit tariffs, while inventories last, higher prices below that tariff’s rate;

2) for single-digit tariffs on goods still economically viable post-tariffs, higher prices up to the tariff’s rate; and

3) for single and double-digit tariffs on goods no longer economically viable, a multiple of the pre-tariff price for tariff-evading goods.

Triple-I remains committed to keeping abreast of these and other developments crucial to the insurance industry’s future. For more information, we invite you to stay tuned to our blog and join us at JIF 2025.

Proposed rules linking traffic violations to higher insurance premiums are under consideration at present. Stricter rules for traffic violations are also being proposed. Experts anticipate that premium pricing might involve a tiered model based on pending challans, potentially using telematics for risk assessment. However, there are valid concerns regarding inflated premiums in cases where challans have been erroneously and wrongfully generated.

Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that impede progress, according to the most recent Triple-I Issues Brief.

Like many states, California has suffered greatly from climate-related natural catastrophe losses. Like some disaster-prone states, it also has experienced a decline in insurers’ appetite for covering its property/casualty risks.

But much of California’s problem is driven by regulators’ application of Proposition 103 – a decades-old measure that constrains insurers’ ability to profitably write business in the state. As applied, Proposition 103 has:

Kept insurers from pricing catastrophe risk prospectively using models, requiring them to price based on historical data alone;

Barred insurers from incorporating reinsurance costs into pricing; and

Allowed consumer advocacy groups to intervene in the rate-approval process, making it hard for insurers to respond quickly to changing market conditions and driving up administration costs.

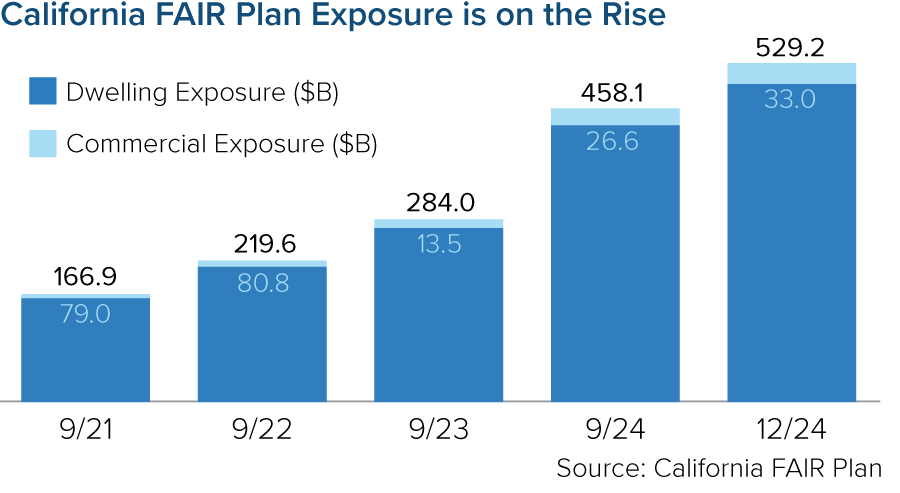

As insurers have adjusted their risk appetite to reflect these constraints, more property owners have been pushed into the California FAIR plan – the state’s property insurer of last resort. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for larger homeowners, condominium associations, homebuilders and other businesses.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to alleviate these pressures. The strategy has generated positive impacts, but it continues to meet resistance from legislators and consumer groups. And, regardless of what regulators or legislators do, California homeowners’ insurance premiums will need to rise.

The Triple-I brief points out that – despite the Golden State’s many challenges – its homeowners actually enjoy below-average home and auto insurance rates as a percentage of median income. Insurance availability ultimately depends on insurers being able to charge rates that adequately reflect the full impact of increasing climate risk in the state. In a disaster-prone state like California, these artificially low premium rates are not sustainable.

“Higher rates and reduced regulatory restrictions will allow more carriers to expand their underwriting appetite, relieving the availability crisis and reliance on the FAIR plan,” said Triple-I Chief Insurance Officer Dale Porfilio.

With events like January’s devastating fires, frequent “atmospheric rivers” that bring floods and mudslides, and the ever-present threat of earthquakes – alongside the many more mundane perils California shares with its 49 sister states – premium rates that adequately reflect the full impact of these risks are essential to continued availability of private insurance.