In India, you can easily check your car insurance details online through platforms such as the Parivahan Portal, IIB Portal, mParivahan app, and state RTO websites. These government-run resources allow you to quickly access your vehicle’s insurance status, policy issuer, and validity by entering the registration number.

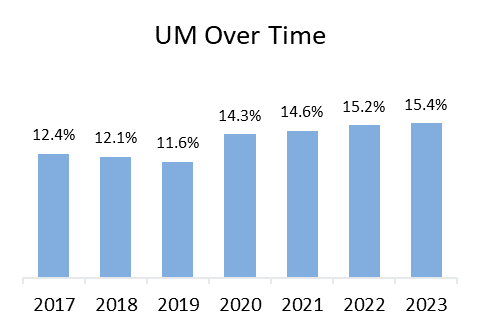

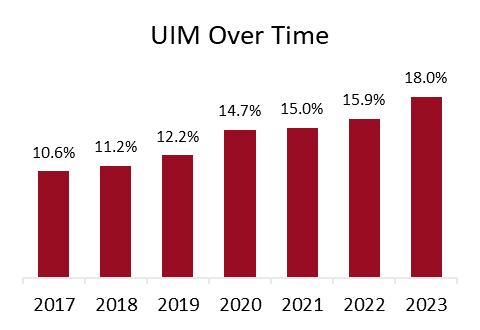

In 2023, despite nearly universal legal requirements to have auto insurance, more than one in seven drivers (15.4 percent) nationally were uninsured, and more than one in six drivers (18.0 percent) were underinsured, according to the new report, Uninsured and Underinsured Motorists: 2017–2023, by the Insurance Research Council (IRC), affiliated with The Institutes. Across the fifty states and the District of Columbia, one in three drivers (33.4 percent) were either uninsured or underinsured in 2023, a 10 percentage point increase in the combined rate since 2017.

Using data submitted by 17 insurers — representing approximately 55 percent of the private passenger auto insurance market countrywide — this latest report estimated the prevalence of uninsured (UM) and underinsured (UIM) by comparing the frequency of UM claims and UIM claims, respectively, to the frequency of bodily injury (BI) claims. Findings included an analysis of trends and contributing factors to variations in UM and UIM rates across states.

The IRC analyzed UM, UIM, and BI liability exposure and claim count data from participating companies for 2017 through 2023. Because of the disruption of the pandemic shutdowns, the changes over time were split into three periods (details outlined in the report).

Key IRC findings include:

UM rates varied substantially across the nation (50 states and the District of Columbia)

Nearly every state saw a rise in the UM rate in 2020 with the onset of the pandemic, but the experience from 2020 to 2023 was mixed.

Every state, except for New York and the District of Columbia, experienced a rise in UIM rate between 2017 and 2023.

Many states with high UM rates often also have high UIM rates. However, some jurisdictions, such as Nevada and Louisiana, combine below-average UM rates with high UIM rates, while others, such as the District of Columbia, have high UM rates but low UIM rates.

Several factors, including economic factors, insurance costs, and state insurance laws and regulations, are associated with variations in UM and UIM rates across states.

After the initial shock of the pandemic, the UM rate increased steadily.

Before the disruption of the COVID-19 pandemic, UM rates were falling in most states. From 2017 to 2019, only 11 jurisdictions saw an increase. UM claim frequency fell slightly in 2020 to 0.11 claims per 100 insured vehicles, but the decline was much smaller than the drop in BI claim frequency. UM claim frequency recovered quickly and, in the years since 2020, has grown faster than BI claim frequency (39 percent compared with 29 percent).

As a result, the UM rate has increased steadily, reaching 15.4 percent in 2023. The range of the UM rates spanned from a low of 5.7 percent in Maine to a high of 28.2 percent in Mississippi. Outliers include eight states with UM rates above 20 percent and 11 states with rates lower than 10 percent.

States with above-average BI claim frequency and UM claim frequency tended to have higher UM rates. Yet, some states with low UM claim frequency rates have a relatively high UM rate. In Michigan, for example, strict no-fault rules limit the number of BI claims, so the ratio of UM-to-BI claim frequencies is high. Lower UM rates tended to occur in states with higher income, lower unemployment rates, lower insurance expenditures, low minimum limits, and a lack of stacking provisions.

UM rates were higher in states that don’t require UIM coverage. In 2023, the UM rate was 14.9 percent in states that do not require UIM insurance, compared with 11.6 percent in states that require it. Where UIM coverage isn’t required by law, UM rates were significantly higher in the years captured in this study, with the rate in 2023 at 18.9 percent in states that don’t require UIM insurance, compared with 13.3 percent in states that require it.

Nearly one in five accidents with injuries involved losses more than the at-fault driver’s coverage limits.

Over the study period, nearly every jurisdiction experienced an increase in its UIM rate. The only exceptions were a small decline (0.9%) in the District of Columbia and a 6.6 percent decline in New York. The largest increase occurred in Colorado, where the UIM rate rose 24.4 percentage points. Other states with above-average increases included Michigan, Kentucky, and Georgia.

UIM claim frequency showed a small increase between 2017 and 2019 before dropping slightly in 2020. In the years since the onset of the pandemic, with the severity of auto injury claims on the rise, UIM claim frequency has increased markedly, reaching 0.17 claims per 100 insured vehicles in 2023. Since 2020, the growth in UIM claim frequency was double the growth in BI frequency. As a result, the UIM rate has increased significantly, rising to 18.0 percent in 2023.

IRC analysis showed that characteristics associated with lower UIM rates included higher income, lower unemployment rates, lower insurance expenditures, high or medium minimum limits, lack of stacking provisions, and use of a limits trigger for UIM coverage rather than a damages trigger. States with high UM rates often also have high UIM rates. Florida, Colorado, and Michigan all rank relatively high for both measures, while Maine, Massachusetts, and Nebraska all rank relatively low.

“The increase in UIM rates points to higher UIM premiums in the future, worsening affordability and potentially increasing the likelihood of more uninsured drivers. This demonstrates the complex interconnectedness of these two coverages as insurers protect consumers from insufficient coverage by at-fault drivers,” said Dale Porfilio, president of the IRC and chief insurance officer at theInsurance Information Institute (Triple-I).

While state laws regarding mandatory requirements for uninsured and underinsured motorists vary, nearly all states have a legislation framework that requires all drivers to have some auto liability insurance to drive a motor vehicle. Drivers in most states are also required to purchase additional protection to provide coverage if the at-fault driver cannot afford to pay for the damage they caused. However, legislators in several states have enacted “no pay, no play” laws, which ban uninsured drivers from suing for noneconomic damages such as pain and suffering. A handful of states have programs to assist lower-income drivers, and drivers can check with their state’s insurance division to see if they are eligible.

Insurance affordability in Georgia is dwindling as claim frequency and insurer costs soar, according to the latest issue brief from Insurance Information Institute (Triple-I), Trends and Insights: Georgia Insurance Affordability.

Given the state’s below-average income vs. above-average insurance expenditures, Georgia ranks 42nd on the list of affordable states forhomeowners insurance and 47th (plummeting from the 2006 high of 27th) forpersonal auto affordability, according to reports by the Insurance Research Council. This brief provides an overview of how several factors, including skyrocketing costs from litigation, pose risks to coverage affordability, availability, and other potential economic outcomes for Georgia residents. Tort reform is discussed as a legislative solution to the challenge of legal system abuse – excessive policyholder or plaintiff attorney practices that increase costs and time to settle insurance claims.

The Georgia insurance market grapples with multiple risk factors

From 1980–2024, Georgia was impacted by134 confirmed weather/climate disaster events in which losses exceeded $1 billion each. At least 38 of those events happened in the last five years, with 14 in 2023. Homeowners in Georgia’s most climate-risk-vulnerable counties, such as the coastal and most southern parts of the state, can face double-digit premium hikes or nonrenewals. Also, data indicates the rate of underinsured motorists in Georgia is twice as high as the national average, and the rate of uninsured motorists is 25 percent higher. Injury claim severity in the state is slightly higher than in the rest of the country.

Data indicates that litigation costs have become a pervasive concern for risk management.

Rising claim frequency and litigation costs put coverage affordability and availability at risk. For example, the IRC findings across personal auto lines show a dual trend in Georgia of increased claims and litigation. Property damage liability claims per 100 insured vehicles are 15 percent higher, and relative body injury claims frequency is 60 percent higher. According to IRC, the rate for private passenger litigation in Georgia is nearly three times that in the median state.

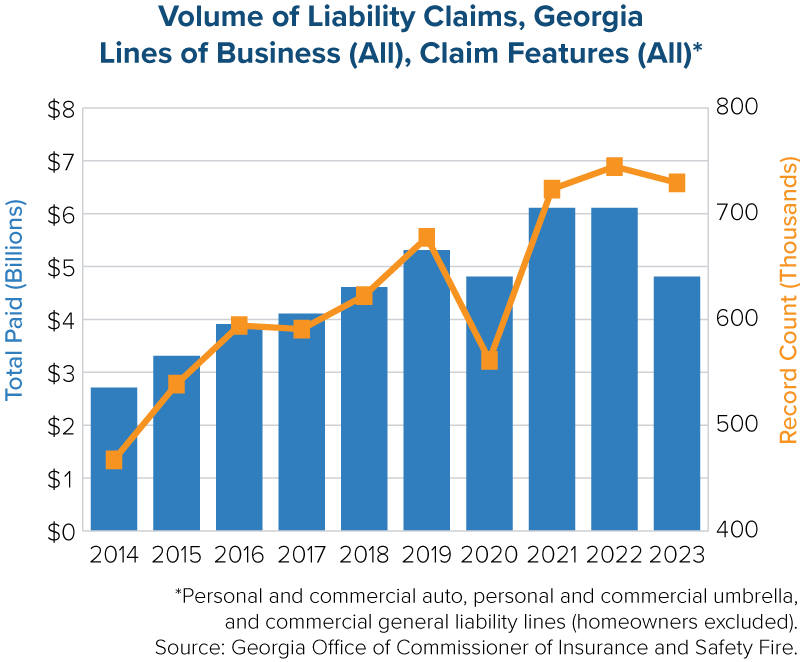

The Georgia Office of Commissioner of Insurance and Safety Fire (“OCI”) reviewed all lines across personal and commercial auto, personal and commercial umbrella, and commercial general liability (homeowners liability was excluded). The five-year average count for liability claims increased 24.9 percent (2014 – 2018 at 583,756 vs. 2019-2023 at 729,191). A rising percentage of claims with payment are full-limit claims, and the OCI analysis indicates litigation is driving that increase. While costs rose for both litigated and non-litigated claims, the number of claims with legal involvement dominated paid indemnity for most lines of business, and litigated claims comprised a growing portion of the total paid indemnity.

Attorneys appear to have revved up their mining for lawsuits in Georgia. Law firms spent $160 million on advertising in Georgia, according to preliminary data from the American Tort Reform Association (ATRA). Outdoor ads for lawsuits increased by 119 percent in GA during that time. It might not be a surprise then to see that the Georgia OCI report shows legal (attorney involved) claims dominated Personal Auto claims for Bodily Injury, comprising 62 percent of claims and 86 percent of total indemnity paid for closed claims in Accident Year 2023. A review of losses of $1 million or more by accident year that have closed during the 2014 to 2023 period shows that each accident year cohort surpasses the count from the previous accident years.

Recently introduced state tort reform legislation may help to stabilize insurance costs.

Analysts estimate that litigation costs Georgia residents $880 million annually, or an average of $1,415 per resident. Sean Kevelighan, Triple-I CEO, says “understanding how these trends drive up costs and identifying policy levers for tort reform legislation can ultimately bring positive outcomes for Georgia’s economy and its consumers and business owners.”

As part of our commitment to educating stakeholders, Triple-I has launched a multi-faceted campaign to raise awareness of the mounting costs oflegal system abuse in Georgia and other states. We invite you to view thevideo statement by our CEO Sean Kevelighan, interviews capturing the opinions of consumers about legal system abuse, and read the full issue brief, Trends and Insights: Georgia Insurance Affordability.

Road safety efforts in Europe offer numerous examples and success stories from which U.S. jurisdictions are learning. In the latest Triple-I Executive Exchange, MAPFRE USA President and CEO Jaime Tamayo sat down with Triple-I CEO Sean Kevelighan to discuss these learnings from an insurance perspective.

“In Europe, road-related fatalities are significantly lower than in the U.S., and we wanted to get a better understanding as to why,” Tamayo said. “We brought together leading experts and policymakers from Europe and the U.S. in transportation, urban planning, public health, and technology to discuss ways in which we can improve policies, innovation, enforcement, and education around safe driving.”

Through its charitable foundation, Fundación MAPFRE, the Spain-based reinsurer is dedicated to “Vision Zero” – a movement begun in Sweden in 1997 with a goal of eliminating traffic fatalities and injury-sustaining crashes. In connection with exporting this effort to the United States, Mapfre for more than 20 years has sponsored a program for the Massachusetts Department of Transportation that consists of a fleet of vehicles that patrol main highways and thoroughfares in the state, helping stranded motorists get back on the road.

“The program has been a great success,” Tamayo said, “covering over 30 million miles of road since its inception.”

In addition to Massachusetts, Vision Zero has been taking hold in communities across the United States, including metropolitan areas such as New York City, Los Angeles, and Portland, Ore.

In Portland, several data points are helping government officials better understand how to reduce traffic fatalities and injuries, including a high percentage of pedestrian crashes occurring because of long distances between marked crossings. Portland has taken the initiative, building “a system to protect pedestrians includes frequent safe crossings, street lighting, a cultural acceptance of slower speeds and people educated about how to interact safely on the streets.”